According to statistics, the price trend of domestic paraxylene market rose in 2018, with an average price of 7 300 yuan/ton at the beginning of the year and 8 500 yuan/ton at the end of the year. The annual increase rate was 16.44%. From the price trend chart, it can be seen that the highest price of domestic PX appeared in the early October, the highest price was 11 000 yuan/ton, the lowest price appeared at the beginning of the year, the lowest price was 7 300 yuan/ton, and the biggest amplitude was 50%. 68%. Overall, the domestic market price of p-xylene is still in an upward trend, which is the result of the joint influence of domestic and foreign factors.

In 2018, China's PX production capacity was 14.015 million tons, but the annual start-up rate was about 7.1% and the total output was about 9.95 million tons. However, the total import volume from January to October was 13.018 million tons. Overall, PX external dependence was as high as 60%. PX external price was the most important factor affecting the domestic market price of paraxylene.

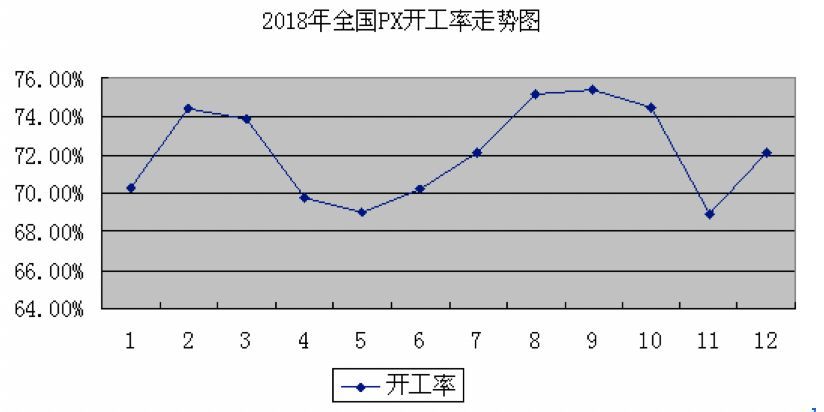

Review of PX Market in 2018

According to the annual domestic market price trend chart and PX external price trend chart, PX market price trend can be divided into three stages: the first stage is from early January to the end of July, PX market price fluctuation stage; the second stage is from early August to mid-October, PX market price increases substantially; the third stage is from mid-October to the end of 2018, PX market price declines sharply.

The first stage is from the beginning of January to the end of July. The domestic market price of PX has been maintained at about 7,500 yuan/ton. From the point of view of product supply, the domestic PX start-up rate maintained about 70%, the domestic plant with 1.6 million tons of production capacity in Fuhai was in overhaul, the Urumqi petrochemical plant started about 50%, the other plants started normally, and the domestic market price trend of p-xylene was relatively stable. But for the domestic PX market, the greater import dependence is the normal of PX products, so the price of external market directly affects the domestic market price of p-xylene. The price of PX external market has been maintained at 900-1000 US dollars/ton CFR Taiwan. The fluctuation of external price is a major support for the domestic market of p-xylene.

From the industrial chain point of view, the first stage of crude oil market has maintained a narrow range of shocks, crude oil prices fluctuated around the $60-70 range, crude oil prices can maintain a relatively high stable operation for a period of time, high crude oil prices have become the cost support of the PX market, so the domestic market price of paraxylene has been maintained at 7500-8000 yuan/ton. The downstream PTA market trend is also relatively stable. The PTA market price has been maintained at around 5750 yuan/ton. In addition, the domestic start-up rate has maintained a high level. The PTA start-up rate is about 75%, the polyester start-up rate is about 85%, the textile start-up rate in Jiangsu and Zhejiang is about 76%. The higher start-up level of downstream PTA Market and polyester industry is a good support for the price of PX market, and the price of PX market remains volatile. Trend.

The second stage is from the beginning of August to the middle of October, when the price of PX market rises sharply. The price of domestic market rises sharply from 8300 yuan/ton to 11000 yuan/ton, an increase of 32 yuan/ton.53%, the sharp rise in domestic market price of paraxylene is mainly the result of the joint influence at home and abroad. August-October is the sales peak season of domestic textile industry. The domestic PX start-up rate is less than 70%. Tenglong Aromatic Hydrocarbon Unit is still in the stop state. Pengzhou Petrochemical Unit is stopped and repaired. Yangtze Petrochemical PX Unit is running normally, Jinling Petrochemical Unit is running smoothly, Qingdao Lidong Unit is running at full load, Qilu Petrochemical Unit is running normally, Urumqi Petrochemical Unit is operating at 50% or so, and in China. Toluene supply is normal, driven by the ups and downs of the rally, domestic market prices rose sharply. Sinopec's PX settlement price rose by 2810 yuan/ton to 10950 yuan/ton in August-September. Sinopec's settlement price rise is a big boost for domestic p-xylene prices.

During this period, international crude oil prices rose sharply. During this period, WTI crude oil prices once rose to a high level of $75 per barrel. On the one hand, European and American countries imposed sanctions on Iran. The Iranian problem led to the anticipated decline in crude oil supply. Western sanctions had a great impact on the supply of Iranian crude oil. As a result, the global market reduced its supply by about 1.4 million barrels per day, compared with that of Libya last year. The supply is equivalent to OPEC's production reduction, and the price of crude oil keeps rising.

On the other hand, the decrease of crude oil inventory leads to the decrease of on-site supply and the continuous rise of crude oil prices. PX external price is sustained by the rise in crude oil prices. By mid-October, PX external price had risen sharply by 400 US dollars/ton to 1380 US dollars/ton CFR Taiwan. The external price has a certain guiding role for the domestic market of paraxylene. The external dependence of paraxylene is as high as 60%, and the higher external price is a good profit for the domestic market of PX.

In addition, PTA market prices continue to rise downstream, domestic PTA market prices have risen sharply to 9250-9300 yuan near self-lifting, and the start-up rate has also risen to varying degrees. PTA start-up rate is about 80%, polyester start-up rate is about 90%, Jiangsu and Zhejiang textile start-up rate is about 80%, autumn is the peak season of textile industry sales, downstream PTA Market prices have risen, together with the end textile industry quotations. To be positive, PX and PTA market prices have risen to varying degrees due to downstream favorable support.

The third stage is from mid-October to the end of 2018. The price of PX market has fallen sharply. The domestic starting rate of PX has been maintained at about 70%. The domestic self-sufficiency rate is seriously insufficient. The larger import dependence is the normal state of PX products. Crude oil prices fell sharply in the fourth quarter. Domestic paraxylene prices fell sharply due to the influence of raw material market. Domestic market prices fell from 11,000 yuan/ton to 8,500 yuan/ton. Generally speaking, the change of external price is an important factor affecting the domestic market price of p-xylene. As of December 24, the closing price of Asian region was US$1003/ton CFR Taiwan. The external price fell by 350 US dollars/ton. The sharp decline of external price was a big shortfall of domestic PX price.

97% of domestic p-xylene is used to produce PTA, and the overall domestic PTA market starts at about 65%. The demand for PX has been in a high state. A sharp decline in downstream PTA is also a negative impact on the p-xylene market. WTI crude oil prices fell sharply in the fourth quarter of 2018. The closing price of WTI was at the level of US$42 per barrel by the end of the year. The sharp decline in crude oil prices has lost strong cost support for the downstream chemical market, and the price of PX market has fallen sharply. Downstream PTA market prices have declined. As of December 25, PTA market prices in East China were 6300 yuan/ton, down 32 yuan from 9300 yuan/ton in early October.2%. In addition, the downstream polyester terminal starts to maintain more than 80% of the level, Jiangsu and Zhejiang textile start-up rate maintained about 70%, downstream terminal industry sales declined, PX market prices continued to decline.

Prospects for PX Market in 2019

In 2019, domestic PX was put into production in large quantities, and the inflection point of supply and demand was expected to appear at 6% supply growth rate: PTA supply was expected to reach 42.48 million tons in 2019, corresponding to PX demand of 28.03 million tons, compared with the additional demand of 1 million tons in 2018. From the end of 2018 to 2019, the domestic production capacity is expected to increase by 11.3 million tons per year, most of which are postponed for 18 years. Hengyi Petrochemical's 1.5 million tons of PX capacity in Brunei is scheduled to be launched in the second quarter of 2019, while other Asian countries have no new capacity yet, with a total additional capacity of 12.8 million tons. According to the conversion of production time, domestic PX production is expected to increase by 3.6 million tons in 2019, PX imports will be reduced to the level of 2017, and the import substitution process will begin. Supply is expected to grow by 6% in 2019, exceeding new demand and breaking the tight balance between supply and demand in 2018. Overall PX shows loose supply.

The profit of PX-naphtha is expected to gradually move down to PTA-PX in 2019 to create profit space. However, considering the impact of oil prices, we expect that PX production will increase by 6%, PTA production by 4% and polyester production by 7% in 2019. PTA in the middle reaches has the least additional capacity, and will continue to maintain tight supply-demand balance in 2019. PX in the upstream will release domestic capacity and gradually realize import substitution, with inflection point ushering in loose supply. From the perspective of supply and demand, we believe that PX, PTA and filament in 2019 will be difficult to reproduce the high price in 2018. However, due to the imbalance of supply and demand structure between upstream and downstream of the industrial chain, the price gap of PX-naphtha, PTA-PX and polyester filament-PTA will be reconstructed and the profit space of the industry will be established. PX prices are expected to decline in 2019, PX-naphtha profits will gradually move down to PTA-PX, PTA-PX price spread will expand.

It is expected that in 2019, even though the nominal demand growth rate of polyester is significantly lower than that in 2018, the supply and demand of polyester filament and PTA are still tight, and profits are expected to remain high. PX-naphtha profits will gradually move down to PTA-PX, from which the downstream industry as a whole will benefit.